The Tariff Landscape in 2026

Chinese electric vehicle manufacturers face the most challenging trade environment in their history. The United States has maintained 100% tariffs on Chinese-built EVs throughout 2026, effectively closing the world's second-largest automotive market to Chinese imports. The European Union, following the conclusion of its anti-subsidy investigation in October 2025, imposed tariffs ranging from 17% to 36% depending on the manufacturer's level of cooperation with the investigation. Even emerging markets like India and Turkey have erected tariff barriers to protect domestic industries.

Yet Chinese EV exports continue to grow. Total exports reached 350,000 units in Q1 2026, up 47% year-over-year, as manufacturers adapt their strategies to circumvent, mitigate, or simply absorb tariff costs. The response involves three parallel strategies: offshore manufacturing, market diversification, and premium brand positioning.

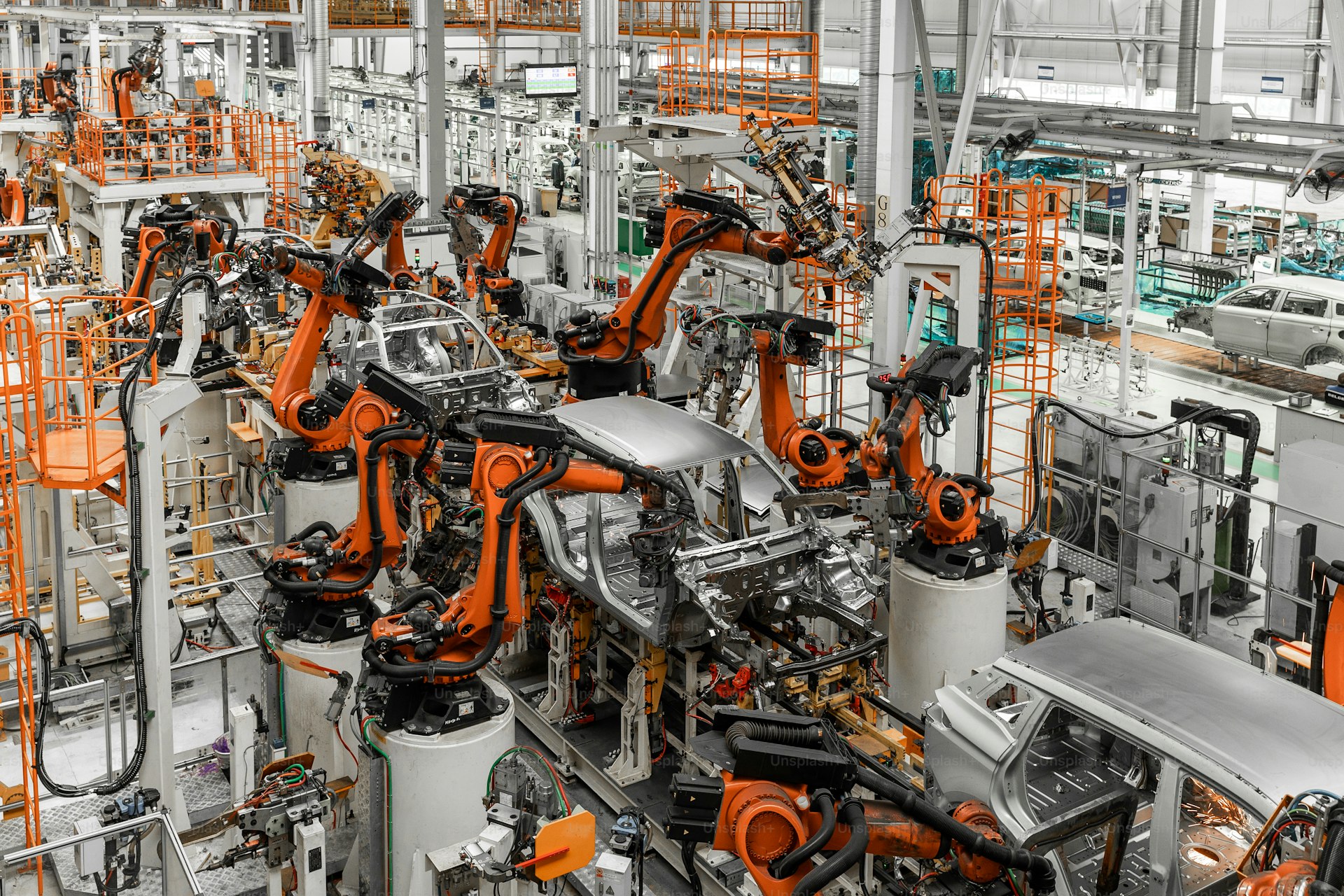

BYD: The Factory-Building Blitz

BYD has pursued the most aggressive offshore manufacturing strategy of any Chinese automaker. The company currently operates or is constructing vehicle factories in Hungary, Brazil, Thailand, Indonesia, Uzbekistan, and Mexico, with cumulative overseas production capacity expected to reach 1.2 million vehicles per year by 2028.

The Hungarian factory near Szeged represents BYD's most strategically important facility. The plant, which began trial production of the Atto 3 and Dolphin in April 2026, will serve as the company's primary supply base for the European market. By manufacturing within EU borders, BYD avoids the 17% tariff applied to Chinese-built EVs and can qualify as a "domestic producer" for the purposes of national EV incentive programs in France, Germany, and Italy.

However, the tariff question remains complex even for European-built BYDs. The EU's rules of origin requirements, part of the EU-China trade framework, stipulate that at least 55% of a vehicle's value must be produced within the EU or countries with free trade agreements to qualify for tariff-free intra-EU trade. BYD's Hungarian plant currently sources approximately 40% of its components locally, with batteries and power electronics shipped from China. The company is investing in a battery pack assembly facility adjacent to the Szeged vehicle plant to increase local content.

BYD's Brazilian factory in Camaçari, Bahia state, has proven particularly valuable for expanding into Latin America. The plant, which produces the Yuan Plus and Dolphin for the Brazilian market, also serves as an export hub for Argentina, Chile, and Colombia. Brazil's Mercosur trade bloc membership gives BYD tariff-free access to a combined market of over 260 million consumers.

Geely and SAIC: Multi-Brand Strategies

Geely Holding Group has taken a different approach, leveraging its portfolio of acquired and invested brands to bypass trade barriers. The company's Swedish subsidiary, Volvo Cars, already manufactures EVs in Europe and the United States. Polestar, now effectively Geely-controlled after Volvo reduced its stake, produces the Polestar 3 in South Carolina and the Polestar 4 in South Korea through Renault Korea Motors.

Zeekr, Geely's premium EV brand, has adopted a "local assembly" model. Rather than building full factories in each market, Zeekr partners with contract manufacturers for final assembly. The Zeekr X is assembled in a former Magna Steyr facility in Graz, Austria, for the European market, while the Zeekr 001 is assembled in Vietnam for Southeast Asian distribution. This asset-light approach reduces capital risk while providing tariff circumvention.

SAIC Motor, China's largest state-owned automaker, has focused on the Morris Garages (MG) brand as its primary international vehicle. The MG4 and MG ZS EV have become among the best-selling EVs in the UK and Australia, benefiting from MG's brand heritage in those markets. However, SAIC faces the highest EU tariff at 36%, having been deemed "non-cooperative" in the EU's subsidy investigation. The company is urgently constructing a factory in Spain to avoid these duties, targeting production start in Q3 2027.

Market Diversification Strategy

Facing barriers in the US and EU, Chinese manufacturers have aggressively diversified their export destinations. Southeast Asia has emerged as the primary beneficiary, with EV sales in Thailand, Indonesia, Malaysia, and Vietnam growing from negligible levels in 2022 to representing 12% of the total new car market in Q1 2026.

Thailand has become the hub of Chinese EV manufacturing in the region, with BYD, Great Wall Motor, SAIC, and NETA all operating factories in the kingdom. The country's EV 3.0 incentive package provides cash subsidies of 50,000 to 150,000 baht per vehicle for locally produced EVs, effectively offsetting any tariff advantage that Japanese or European competitors might have.

The Middle East has also emerged as a growth market. BYD and Geely have established distribution partnerships across the GCC states, with the UAE, Saudi Arabia, and Israel representing the largest markets. Saudi Arabia's Public Investment Fund has discussed the possibility of co-investing in a Saudi-based EV factory with Chinese partners, though no deal has been finalized.

Africa, while representing a small absolute market today, is viewed as a long-term growth opportunity. Ethiopian, Moroccan, and South African governments have approached Chinese EV makers offering tax holidays and land grants for local assembly. BYD announced in April that it would establish a CKD assembly plant in Ethiopia for the Seagull and Dolphin models, with initial annual capacity of 10,000 units.

The Response from Western Manufacturers

Western automakers have responded to the Chinese export push with a combination of competitive and defensive measures. Ford and GM have accelerated their own affordable EV programs, with Ford announcing a $3 billion investment in a sub-$25,000 EV platform codeveloped with a South Korean partner, while GM has reprioritized the Chevrolet Bolt successor.

Volkswagen's response has been notably different. The German automaker has deepened its partnership with XPeng, moving beyond the initial co-development agreement announced in 2024. The two companies are now co-developing two mid-size EVs for the Chinese market and one global model designed for European and North American sale. XPeng's software expertise and efficient platform architecture complement Volkswagen's manufacturing scale and brand reach.

The European Commission has signaled that tariffs are not a permanent policy but a bridge measure to protect the European auto industry while it transitions to EV production. The commission expects European OEMs to achieve competitive EV cost structures by 2029, at which point tariffs on Chinese imports could be progressively reduced. Whether European manufacturers can meet this timeline with labor costs three to four times higher than Chinese counterparts remains an open question.

The Geopolitical Dimension

EV trade has become intertwined with broader geopolitical tensions between China and Western nations. Battery supply chain security, rare earth mineral processing, and data sovereignty for connected vehicles have all become points of friction. The US Department of Commerce's proposed rule on connected vehicle data security, still pending as of May 2026, could effectively ban Chinese-branded connected vehicles from US roads regardless of where they are assembled.

The Chinese government, for its part, has signaled its commitment to supporting the global expansion of its EV industry. Export credit agencies at the China Export-Import Bank and China Development Bank have extended preferential financing for overseas factory construction. Diplomatic outreach in Southeast Asia, Latin America, and Africa has included EV cooperation as a central component of bilateral trade discussions.

The tariff battle represents the latest chapter in the globalization of the automotive industry. Chinese manufacturers, having achieved cost and technology leadership in EVs within their home market, are determined to become global players. The question is whether trade barriers will permanently fragment the global auto market into tariff-protected regional blocs or whether they will serve as a temporary adjustment mechanism as the industry restructures around Chinese manufacturing competitiveness.